Fintech apps pay a few of the highest prices per set up (CPIs) in cellular; Mapendo’s 2025 Price per Set up report places the monetary class on the prime of each vertical it benchmarks. That payout premium makes fintech a disproportionate goal for set up fraud, and the implications prolong properly previous wasted finances. Fraudulent installs corrupt the client intelligence behind danger fashions, know your buyer (KYC) and anti-money laundering (AML) information, and regulatory reporting, creating compliance vulnerabilities that invite scrutiny.

The assaults cut up into two distinct classes. The primary is fabricated installs: bots, emulators, and system farms producing set up occasions with no actual consumer behind them. The second is attribution hijacking, the place the set up is actual however a fraudster steals credit score for it. Each corrupt your acquisition information by completely different mechanisms that require completely different defenses. Treating them as one undifferentiated downside is why most fraud methods fall brief.

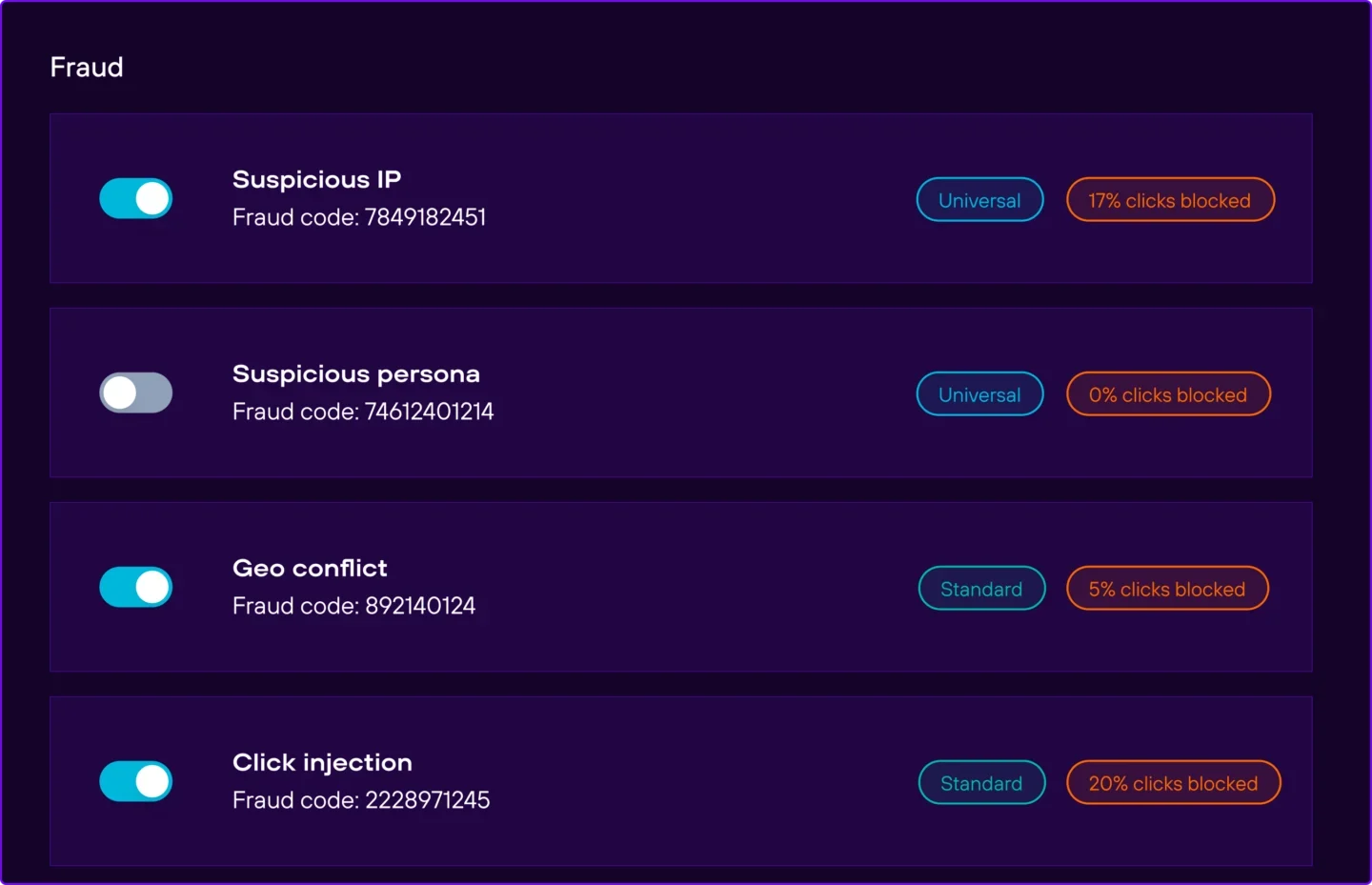

As a result of fraud detection is constructed into the attribution platform fairly than layered on prime of it, suspicious installs get flagged earlier than they’re ever credited to a paid channel, with no reconciliation lag and no separate vendor handoff.

Understanding set up fraud in fintech

Set up fraud splits into the 2 classes we simply coated, faux exercise and attribution hijacking, and every one operates by a number of distinct assault vectors. Right here’s how the commonest ones work and which class they fall into.

Click on injection and click on spamming

Click on injection and click on spamming are two of probably the most pervasive types of attribution hijacking. Each click on fraud strategies manipulate the attribution window to steal credit score for reputable consumer installs by essentially completely different mechanisms.

Click on injection exploits Android’s set up broadcast system by listening for app set up occasions and injecting a fraudulent click on milliseconds earlier than the set up completes. This permits fraudsters to assert attribution credit score for natural installs they’d no function in producing, diverting your advertising finances away from channels that really drove worthwhile buyer acquisition.

Click on spamming, or click on flooding, takes a volume-based method, producing large numbers of clicks from actual gadgets with none real consumer intent. Fraudsters flood attribution techniques with clicks throughout hundreds of system IDs, betting that some share will finally set up your fintech app organically. Once they do, the fraudster’s latest click on receives attribution credit score, contaminating your information with false indicators about which channels drive actual buyer engagement.

Each techniques look reputable in fundamental dashboards. The tells, which embrace impossibly brief click-to-install instances, irregular click on volumes, and statistical anomalies in conversion charges, solely floor in subtle detection techniques.

SDK spoofing and system emulation

SDK spoofing is probably the most technically subtle type. Fraudsters reverse-engineer attribution protocols and ship fabricated set up information on to measurement platforms, with no actual system and no actual consumer behind it, simply artificial indicators designed to set off payouts.

System emulation takes this additional by creating digital system environments that mimic reputable consumer conduct. Fraudsters use emulators and system farms to simulate tons of or hundreds of distinctive gadgets, every showing to put in your fintech app with:

- Life like system identifiers

- IP addresses

- Behavioral patterns

While you’re paying $50–$200 per set up for certified banking or funding app customers, unhealthy actors have sturdy monetary incentive to good their methods.

Geomasking and geo-spoofed installs

Geomasking is when fraudsters use VPNs, proxies, or location spoofing to disguise the place an set up truly originated. The motive is cross-border arbitrage: ship installs from low-CPI markets whereas billing them as installs from a high-CPI market, or slip emulator installs into tightly geo-restricted fintech campaigns.

Attribution hijacking and natural poaching

Attribution hijacking is the umbrella class for fraud that targets actual installs from actual customers, the place the set up goes to occur anyway however a fraudster intercepts the credit score.

Fintech campaigns additionally face::

- Referrer hijacking, the place malware rewrites the Play Retailer referrer string on Android to overwrite the reputable supply of the set up

- Natural poaching, which systematically targets customers already trying to find your model identify or navigating on to your app retailer itemizing

Fraudulent networks monitor app retailer exercise and hearth attribution occasions after they detect customers viewing your itemizing, successfully claiming natural installs as paid conversions. That is notably damaging in fintech, the place model belief drives important natural acquisition.

Incent fraud

The installs come from actual gadgets, however the customers have no real interest in the product. Downstream, they give the impression of being similar to faux installs: zero retention, no funded accounts, no transactions. In fintech, hid incentivized site visitors burns KYC verification credit score on customers who had been by no means going to finish onboarding.

Incent site visitors, the place customers get rewards or cashback for putting in an app, shouldn’t be fraud by itself. It turns into fraud when a sub-publisher runs incent site visitors on a non-incent marketing campaign and disguises it as organic-quality acquisition.

Cellular advert fraud drains fintech advertising budgets whereas corrupting the info you depend on to make strategic selections.

Buyer acquisition price (CAC) and lifelong worth distortion (LTV)

Buyer acquisition price (CAC) calculations break first. Faux installs rely as acquisitions in your denominator, so your reported CAC understates what actual customers truly price. You suppose you’re buying prospects for $45 when the true price for reputable customers is nearer to $78, which makes each channel look extra environment friendly than it’s and factors finances on the unsuitable sources.

Lifetime worth (LTV) calculations break subsequent, however by a special mechanism. Cohort evaluation averages income throughout everybody counted as a consumer, and bots by no means open accounts, deposit funds, or generate transaction charges. Their zero contribution drags down common income per consumer, which then drags down the LTV determine you employ to set acquisition budgets and forecast cohort economics.

The strategic penalties compound over time:

- Price range misallocation: You double down on fraudulent channels that seem worthwhile whereas ravenous genuinely efficient acquisition sources.

- Valuation distortion: Investor displays showcase consumer acquisition effectivity that doesn’t exist in actuality.

- Retention mannequin failure: Predictive fashions for churn and engagement practice on datasets the place a big share of “customers” by no means existed.

- Marketing campaign optimization paralysis: A/B checks and inventive iterations optimize for fraud patterns fairly than human conduct.

In case your fintech app has a goal LTV of $850 and also you’re unknowingly paying for 10,000 fraudulent installs month-to-month at $50 every, that’s $500,000 in direct waste, and the chance price is much larger when you think about the reputable prospects you may have acquired with correct attribution information guiding your spend.

Danger mannequin contamination and fraud operations burden

Each fraudulent set up in your information pipeline teaches your ML fashions to learn bot conduct as reputable consumer patterns. Safety analysts burn hours chasing artificial identities, whereas precise fraud patterns get tougher to detect as a result of your baseline metrics now not mirror actual customers.

The operational prices compound rapidly:

- KYC verification waste: Your processes run on fraudulent accounts that can by no means full onboarding, burning by identification verification credit and analyst time.

- Product roadmap distortion: Your product workforce makes selections primarily based on engagement information that features bot exercise.

- Downstream system unreliability: Each system that depends on clear attribution information, from personalization engines to credit score danger fashions, produces more and more unreliable outputs.

Regulatory reporting and compliance implications

Public fintechs disclose combination advertising bills in U.S. Securities and Alternate Fee (SEC) filings, and plenty of fintechs report buyer acquisition information internally for board reporting, investor updates, and audit.

The compliance implications span a number of vital areas:

- Advertising spend disclosure accuracy: Faux installs inflate marketing campaign prices with out delivering actual customers, making cost-per-acquisition figures doubtlessly deceptive in monetary statements.

- KYC information high quality: Bots and fraudulent gadgets coming into your funnel pollute the info you employ to determine buyer identification verification baselines.

- Promoting transparency obligations: Rules just like the Common Knowledge Safety Regulation (GDPR) and the California Shopper Privateness Act (CCPA) set a authorized framework for information dealing with and transparency. Fraud corrupts each.

Detecting and stopping faux app installs

Fashionable attribution platforms can establish and block fraudulent installs in actual time, earlier than they contaminate your information.

Technical detection strategies

Efficient detection begins with the behavioral patterns that separate reputable customers from bots. Search for:

- Suspicious conversion time: Fraudulent installs typically full suspiciously quick, typically inside seconds of a click on. Department recommends blocking click-to-install instances underneath 10 seconds.

- Geo conflicts: A click on in a single nation and an set up or in-app occasion out of the country normally indicators VPN, proxy, or location-spoofing fraud.

- System conflicts: When the system on the clicking doesn’t match the system on the set up, the conversion is sort of by no means an actual consumer, since actual customers click on and set up on the identical system.

- Suspicious system patterns: {Hardware} traits, OS configurations, and sensor information assist establish emulators and spoofed gadgets that bots battle to copy convincingly.

- System ID resets: Repeated system ID resets are a trademark of system farms biking the identical {hardware} by new identities to repeatedly declare set up credit score.

- Put up-install engagement: Faux installs hardly ever progress past the app open, exhibiting zero session depth or in-app occasions.

Your detection system ought to constantly monitor these indicators in opposition to historic baselines. In case your typical install-to-registration charge is 40% however a marketing campaign all of the sudden delivers 5%, examine instantly.

Department fraud detection makes use of proprietary algorithms, dynamic guidelines, and statistical sample detection throughout a big pool of information indicators to flag and block suspicious installs earlier than they’re ever credited to a paid channel.

Associate administration and transparency

Expertise received’t repair set up fraud in case your media companions are the supply. Set up baseline efficiency metrics for each associate, tracked per community:

- Set up-to-registration charges

- First-session conduct patterns

- Downstream conversion metrics

While you section by associate, fraudulent sources floor quick. Earlier than including new networks, vet them on the standards beneath:

- Fraud prevention measures: Request detailed details about what every associate has in place.

- References: Ask for references from different fintech advertisers.

- Check budgets: Begin small to validate site visitors high quality earlier than scaling spend.

- Granular reporting: Demand sub-publisher IDs, device-level information, and timestamp data that lets you cross-reference installs in opposition to your personal attribution information.

Networks that received’t present this degree of transparency ought to elevate quick purple flags.

When a sub-publisher’s fraud charge exceeds 15%, open a dialog with the associate about that supply. Above 20%, cease operating their site visitors till they remediate. These thresholds align with Department’s customary fraud suggestions and provide you with a defensible line for pausing spend.

Constructing a complete faux set up protection technique

Fraud prevention is a layered stack, and the attribution layer is the final checkpoint, not the primary. Pre-bid filtering inside demand-side platforms (DSPs) and supply-side platforms (SSPs) blocks suspicious stock earlier than a bid clears. Advert networks rating clicks and impressions in flight. Your attribution platform sees each set up for the time being credit score will get assigned, which is the place Department’s native fraud protection operates, routinely flagging suspicious occasions and providing you with transparency into what was blocked and why.

Set up clear fraud thresholds and automatic responses. Outline the metrics that set off investigations: install-to-registration beneath 15%, irregular set up volumes from particular sub-publishers, or geographic anomalies outdoors your marketing campaign concentrating on. Map threats by severity and assign response protocols, with SDK spoofing and system emulation triggering quick associate suspension and forensic evaluation. When vetting companions, prioritize these with adaptive, algorithm-driven detection. Static blocklists can not maintain tempo with fraud operations that actively examine and engineer round mounted guidelines.

See how Department’s built-in fraud detection retains faux installs out of your attribution information, so each greenback of acquisition spend drives an actual buyer as an alternative of a bot

Continuously requested questions on faux app installs

Fraudulent set up spikes seem disconnected from marketing campaign timing and produce abnormally low downstream conversion charges, whereas monitoring points have an effect on attribution accuracy with out altering consumer high quality metrics.

Study whether or not your set up surge aligns with energetic campaigns, new inventive, or seasonal traits. Additionally analyze post-install conduct: reputable customers progress by onboarding at predictable charges, whereas faux installs present zero engagement past the attribution occasion. Verify for geographic anomalies: If installs all of the sudden focus in areas the place you’re not operating campaigns, or if system distributions shift towards older fashions or obscure producers, fraud is the seemingly perpetrator.

There’s no single threshold that indicators fraud by itself as a result of install-to-registration charges differ closely by fintech sub-vertical and acquisition channels. The fraud sign isn’t absolutely the quantity, it’s the deviation. If one associate’s install-to-registration charge sits properly beneath your personal historic baseline for that channel, or one sub-publisher delivers 8% whereas the remainder of your community delivers 30% to 40%, that’s the sign value investigating.

At all times section by site visitors supply, evaluate in opposition to your personal baselines fairly than common thresholds, and mix the metric with corroborating indicators like click-to-install time and post-install occasion depth earlier than concluding it’s fraud.

Not at all times. It is dependent upon the place within the stack you want protection. Department handles fraud on the attribution layer, the place each set up converges and credit score selections get made. What Department doesn’t do is function upstream of the set up, like pre-bid filtering inside DSPs and SSPs or click on scoring inside advert networks. If most of your spend runs by programmatic show, a devoted pre-bid vendor on prime of your MMP is normally value it. If most runs by MMP-integrated advert networks that rating site visitors upstream, attribution-layer detection plus the community’s personal filtering is normally sufficient.