The monetary companies sector additionally faces increased attribution fraud publicity. Forty p.c of surveyed firms reported being focused by fraud in 2025, with monetary companies organizations experiencing disproportionate publicity, in accordance with Sumsub’s Identification Fraud Report, At $50 to $200+ per certified consumer acquisition in aggressive markets, even a ten% fraud price interprets to a whole bunch of 1000’s in wasted spend yearly.

Attribution fraud hits monetary expertise firms tougher than most verticals. Your clients carry exceptionally excessive lifetime values (LTVs): a single banking app consumer who maintains an account for years represents 1000’s of {dollars} in income. That worth is precisely what makes fintech a goal. Increased consumer values drive increased prices per motion (CPAs), and greater CPAs imply larger payouts per stolen conversion. Fraudsters gather the complete CPA for each fraudulent declare they make

Attribution fraud creates compliance issues distinctive to fintech entrepreneurs by corrupting advertising information and impacting the source-of-truth data regulators anticipate.

What’s attribution fraud, and why are monetary expertise firms prime targets?

Attribution fraud is the deliberate manipulation of attribution information to assign credit score for consumer conversions to a writer or affiliate that didn’t have a job in producing it. Fraudsters exploit monitoring mechanisms to make it seem a supply influenced an set up, sign-up, or transactions they didn’t drive.. It corrupts the efficiency information main entrepreneurs to chop channels which are working and scale ones that aren’t.

Monetary companies clients have exceptionally excessive lifetime values, which makes fintech acquisition funnels a goal for fraudsters. A single stolen conversion can yield outsized payouts.

Final-click hijacking via affiliate and sub-affiliate site visitors

Affiliate and sub-affiliate site visitors is a frequent supply of attribution fraud in fintech. Fraudulent associates monitor consumer conduct and inject themselves into the conversion path instantly earlier than a consumer completes a signup or transaction, claiming credit score for conversions they didn’t drive.

A consumer discovers your fintech app via a model marketing campaign or natural search, downloads it, and begins account creation. Simply earlier than they full registration, a malicious affiliate fires a click on that seems to be the “final contact” earlier than conversion. Your attribution system credit that affiliate, and also you pay a fee for a consumer who was already dedicated to signing up.

Widespread last-click hijacking ways embody:

- Click on spamming: Firing a excessive quantity of clicks so one ultimately strains up with an natural set up the affiliate didn’t drive, usually displaying up as an unusually lengthy click-to-install time

- Cookie stuffing: Dropping monitoring cookies with out real engagement

- Toolbar and browser extension manipulation: Firing affiliate clicks no matter coupon use

- URL parameter injection: Appending affiliate parameters to natural URLs

- Redirect chains: Inserting fraudulent touches earlier than customers attain your touchdown web page

These conversions seem reputable in your reporting as a result of the customers are actual and the installs are real, making it troublesome to differentiate earned from stolen attribution with out refined detection.

Click on injection and SDK manipulation in cell app acquisition

Cellular app acquisition fraud has developed far past easy bot site visitors. Click on injection exploits Android’s broadcast listeners to fireplace fraudulent clicks after a reputable set up has begun however earlier than the consumer opens the app for the primary time. A compromised app already on the consumer’s system detects the set up in progress, then fires a faux click on designed to win last-touch attribution credit score for an acquisition one other channel really drove.

Software program growth equipment (SDK) manipulation takes this menace additional. Fraudsters create modified variations of reputable attribution SDKs or inject code that alters how attribution information is collected. These manipulated SDKs can generate faux set up occasions, modify system identifiers to simulate new customers, alter timestamps to win attribution credit score, and bypass customary fraud detection mechanisms.

UTM parameter spoofing and redirect chain exploitation

UTM parameter spoofing is troublesome to detect as a result of the consumer journey seems technically legitimate, with an actual click on, an actual consumer, and an actual conversion. Fraudsters intercept reputable consumer journeys via redirect chains, strip your unique UTM parameters, and change them with fraudulent ones that credit score a unique supply. The consumer completes their account opening or mortgage utility. The fraudster collects the payout for a conversion they by no means influenced.

This distorts your channel efficiency information and pushes you to chop finances from higher-performing channels.

Detecting attribution fraud in fintech buyer acquisition

Recognizing attribution fraud requires statistical vigilance, behavioral evaluation, and technical safeguards working collectively.

Analyze efficiency anomalies and consumer conduct patterns

Three patterns point out attribution fraud:

Sudden efficiency spikes that don’t match consumer high quality. A site visitors supply delivering 300% extra conversions in a single day with no corresponding marketing campaign change signifies fraud. Respectable progress follows predictable patterns tied to advertising actions. Fraudulent site visitors seems as unexplained surges concentrated round particular companions or channels.

Time-to-conversion patterns. Real fintech customers analysis monetary merchandise earlier than changing. They examine charges, learn evaluations, and consider security measures. Fraudulent conversions usually present unrealistic quick time-to-install or time-to-registration metrics, ceaselessly finishing inside seconds of the attributed click on.

Submit-install engagement. Fraudulent installs hardly ever progress past the preliminary app open. In contrast to actual customers, fraudsters by no means full KYC verification, hyperlink financial institution accounts, or make transactions — so excessive set up volumes from a particular supply paired with near-zero Day 7 or Day 30 retention is a dependable sign that the attribution is being gamed. These customers generate no income and depart no significant behavioral hint.

Determine server-side occasion discrepancies

Server-side occasion discrepancies reveal some of the telling signatures of attribution fraud: the hole between what your client-side monitoring stories and what your server really data. Fraudsters usually concentrate on client-side indicators like clicks and impressions. They’re unable to manufacture downstream occasions that occur in your servers, like account creations, KYC completions, first deposits, or mortgage purposes.

Monitor for:

- Conversion price anomalies, like 500 attributed installs however solely 12 account registrations indicators potential click on injection

- Suspiciously uniform time-to-conversion timing

- Occasion sequence violations, the place occasions fireplace out of order or skip necessary steps

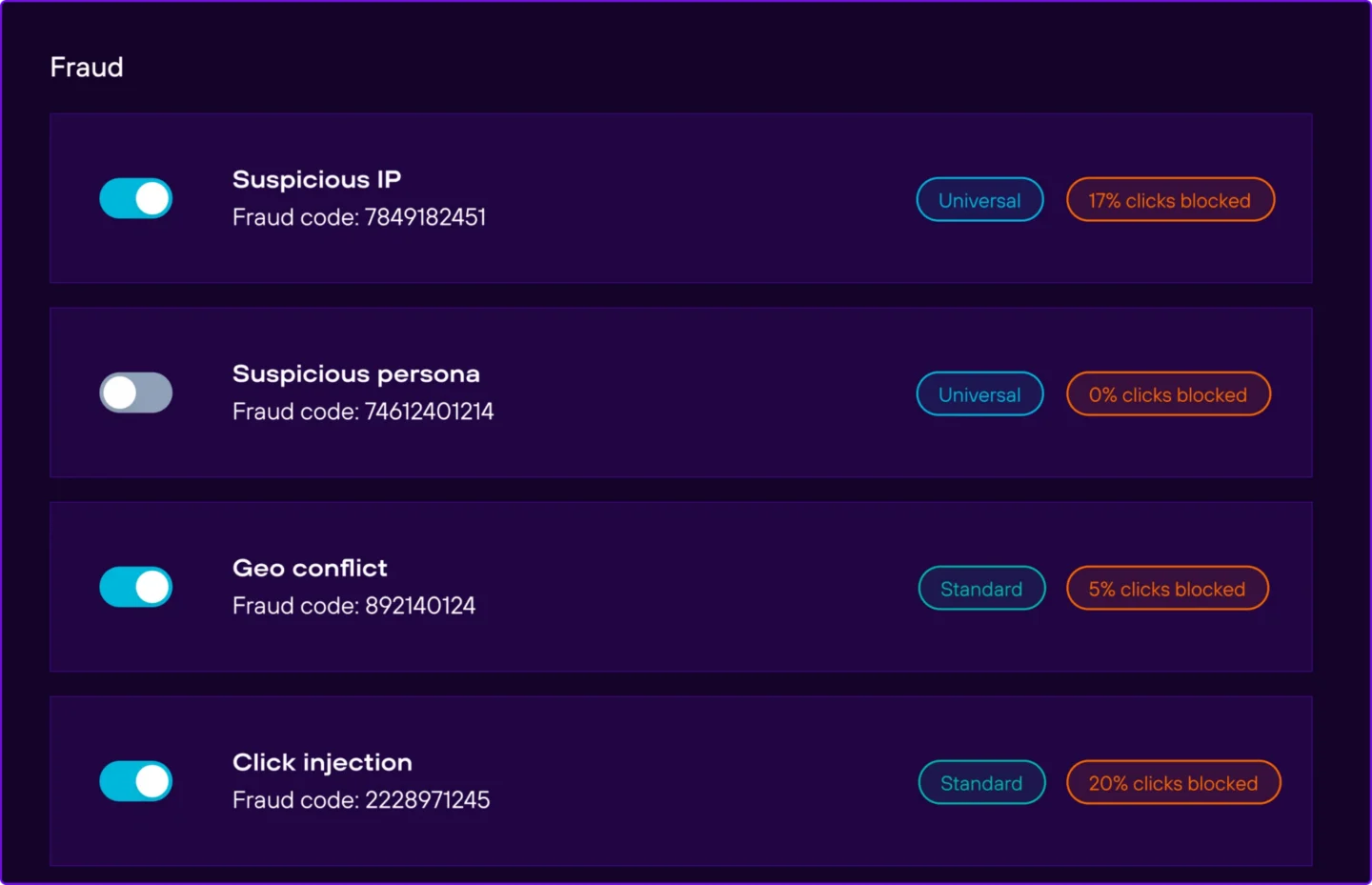

The Department fraud detection platform blocks fraudsters in actual time. It applies configurable guidelines, together with suspicious conversion occasions, system conflicts, geo conflicts, suspicious units. Department catches fraudulent attributions earlier than they distort your dashboard or your spend selections.

Implement measurement design controls

Measurement design controls make it structurally troublesome for fraudsters to govern your information. Three controls ship essentially the most safety:

Sensible attribution home windows. Set attribution home windows to mirror lifelike consumer conduct in fintech. Monetary app customers usually want 24–72 hours to evaluate phrases, full identification verification, and make knowledgeable selections. Tighter home windows cut back the time click on spammers can declare credit score for natural conversions. Pair attribution home windows with suspicious conversion time guidelines that flag installs occurring inside seconds of a click on filters out fraud at each ends of the timing vary.

Clear attribution logic hierarchies. Prioritize deterministic matching over probabilistic strategies, favoring device-level matching and authenticated consumer information over simply spoofed indicators like IP addresses.

Conversion validation guidelines. Require significant in-app actions (account creation, KYC submission, or preliminary deposit) earlier than crediting high-value occasions. Multi-step validation eliminates the chance for fraudsters to say credit score for conversions.

Set up accomplice governance and contract necessities

Advertising and marketing companions will be your strongest allies in preventing attribution fraud. Embed anti-fraud measures into each accomplice contract:

- Prohibit particular ways and specify that companions should not interact in click on injection, set up hijacking, or any type of attribution manipulation.

- Outline efficiency benchmarks that set off fraud evaluations.

- Require granular reporting on site visitors sources and consumer acquisition strategies.

- Construct in monetary penalties for confirmed fraud, together with clawback provisions and tiered penalty methods that make fraud financially unviable.

Deploy technical validation and bot filtering

Technical validation and bot filtering establish fraudulent assaults that measurement controls and accomplice governance don’t catch.

Gadget fingerprinting and behavioral evaluation distinguish reputable customers from bots, analyzing system traits, community patterns, interplay timing, and behavioral sequences.

Server-side validation checks affirm that set up timestamps align with click on time stamps, system identifiers match throughout occasions, and IP addresses correspond to anticipated geographic places.

Actual-time fraud scoring blocks suspicious site visitors instantly slightly than discovering fraud weeks later throughout month-to-month reporting.

For fintech campaigns the place consumer acquisition prices are excessive and compliance necessities are strict, set conservative thresholds: it’s higher to lose a couple of edge-case attributions than to pay for fraudulent conversions.

Constructing a multi-layer attribution fraud prevention framework

A sturdy fraud prevention framework runs in 5 layers:

- Layer 1: Technical validation and filtering. Implement system fingerprinting, bot filtering, and IP popularity scoring to forestall fraudulent site visitors from coming into your attribution information.

- Layer 2: Measurement design controls. Set lifelike attribution home windows, implement probabilistic matching alongside deterministic strategies, and set up clear guidelines for crediting conversions throughout a number of touchpoints.

- Layer 3: Accomplice governance and oversight. Set up efficiency baselines for every accomplice, require transparency into their site visitors sources, and construct penalty clauses for verified fraud into each contract. Common audits establish which relationships ship real worth.

- Layer 4: Steady monitoring and evaluation. Monitor conversion velocity, consumer engagement depth, and post-install conduct to identify anomalies as they emerge.

- Layer 5: Compliance integration. Attribution fraud is a compliance threat. Fraud prevention framework should align with KYC necessities, anti-money laundering protocols, and regulatory reporting requirements.

Widespread questions on attribution fraud in fintech

Attribution fraud targets the credit score project course of for conversions, slightly than fabricating faux customers or clicks. Click on fraud generates faux clicks to empty advert budgets, whereas set up fraud creates faux app downloads. Fraud manipulates reputable consumer journeys to steal recognition for conversions that will have occurred anyway. The customers are actual; they simply didn’t come from the supply claiming credit score.

Attribution fraud exploits the complexity of multitouch attribution. Its monetary impression compounds over time by corrupting your whole advertising technique and misallocating future budgets.

Pause funds to suspicious companions instantly and start a forensic audit of your attribution information. Pull granular information for the previous 30–90 days and study excessive conversion charges, irregular time-to-install patterns, geographic mismatches between click on and set up places, or clusters of installs occurring inside seconds of one another.

- Convene your fraud response crew, together with advertising operations, authorized, compliance, and your attribution platform supplier.

- Tighten your attribution home windows.

- Allow server-side validation for high-value occasions.

- Activate fraud filtering performance.

- Audit your whole accomplice ecosystem.

Shield your fintech advertising investments from attribution fraud

Fintech entrepreneurs who implement complete fraud prevention frameworks achieve clearer efficiency insights, stronger accomplice relationships, and higher information integrity. However provided that the attribution platform beneath can sustain. Each fraudulent conversion that slips via wastes finances, distorts marketing campaign information, and creates potential compliance publicity.

Department delivers fraud safety constructed for the complexity of monetary companies advertising: real-time fraud monitoring, an open-source SDK your safety crew can audit line by line, and cross-channel visibility throughout cell and internet. Clear reporting makes it easy to audit accomplice efficiency, validate marketing campaign outcomes, and exhibit measurement integrity to stakeholders and regulators.

Work with Department to lock down attribution throughout each fintech acquisition channel. The conversions you pay for are the conversions you earned.